Here, we would provide you with a detailed report on what you need to know about a credit-based insurance score.

What Is A Credit-Based Insurance Score?:

The credit-based score also known as the insurance credit score is basically used to determine how probable you are to file for a claim.

This gives insurance companies an idea of how coverage of you would be a risk and also it helps them to decide on your charges for the coverage.

These credit scoring models have been very reliable over the years. According to a 2003 study by the University of Texas, drivers with the worst scores are more likely to file an insurance claim than drivers with good scores.

In some instances, poor credit scores can increase your car insurance rates than DUIs.

A credit-based insurance score can be used to determine other coverage types such as home and renters but you will get a separate score for each insurance type.

LexisNexis insurance company however offers scores that can be used across the board.

States such as California, Hawaii, Michigan, Washington, and Massachusetts do not allow insurers to use credit when setting car insurance rates.

Credit-Based Insurance Score VS. Regular Credit Score

The score used when you apply for a mortgage, credit card or auto loan commonly called VantageScore or FICO credit score is not the same as the insurance credit score.

The determinants however are the same, just measured differently. The basic difference is that a credit score will estimate the likelihood of you paying your debt while the credit-based insurance score finds the likelihood of you filing for an insurance claim.

Regardless of your insurer, the higher your score, the better for you.

Below is a breakdown of how FICO measures insurance credit scores, according to the National Association of Insurance Commissioners (NAIC):

- Outstanding debt (30%)

- Pursuit of new credit(10%)

- Payment history (40%)

- Credit history length (15%)

- Credit mix (5%)

The following could negatively impact your insurance credit score:

- Missing payments

- Having little to no credit history.

- Too many hard credit inquiries

- High credit card balances are commonly known as your credit utilization.

Personal information that cannot be used in determining your credit-based insurance score include;

- Location of residence

- Age

- Gender

- Income and occupation

- Marital Status

- Race

- Religion

Your credit score can be a good gauge for your credit-based insurance score.

What’s A ‘Good’ Insurance Credit Score?

Every insurance company has its own definition of what a good score is. A company might decide that a score of 750 or better unlocks the lowest car insurance rates while another company might just require 700 or better.

Scores come from different credit-reporting companies and those numbers won’t always be weighed on the same plate.

Let’s look at an example of scores and rankings from the LexisNexis website:

- Good: 776 – 997

- Average: 626 – 775

- Below average: 501 – 625

- Less desirable: Under 500

On the website of TransUnion, a good score is around 770 or higher.

Average Car Insurance Rates for Poor Credit

Every insurer has its definition for what a poor insurance credit score is. Using the example above, 625 and lower would be considered poor credit.

The rates for drivers with poor credit are:

- $2,506 per year for full coverage

- $1,078 per year for minimum coverage

The average car insurance for a good driver with very good credit is $1,080 less per year for full coverage and $471 less per year for a minimum coverage comparatively.

Do All Auto Insurers Use Credit-Based Insurance Scores?

A lot of critics say it is unfair to price auto insurance based on a credit score since it cannot determine the accident risk of a driver.

This has come under a lot of probes over the years.

Some insurance is starting to overlook the credit scores; Dillo in Texas has no credit score check. Scouting around for car insurance quotes can help you find lower rates especially when you have poor credit.

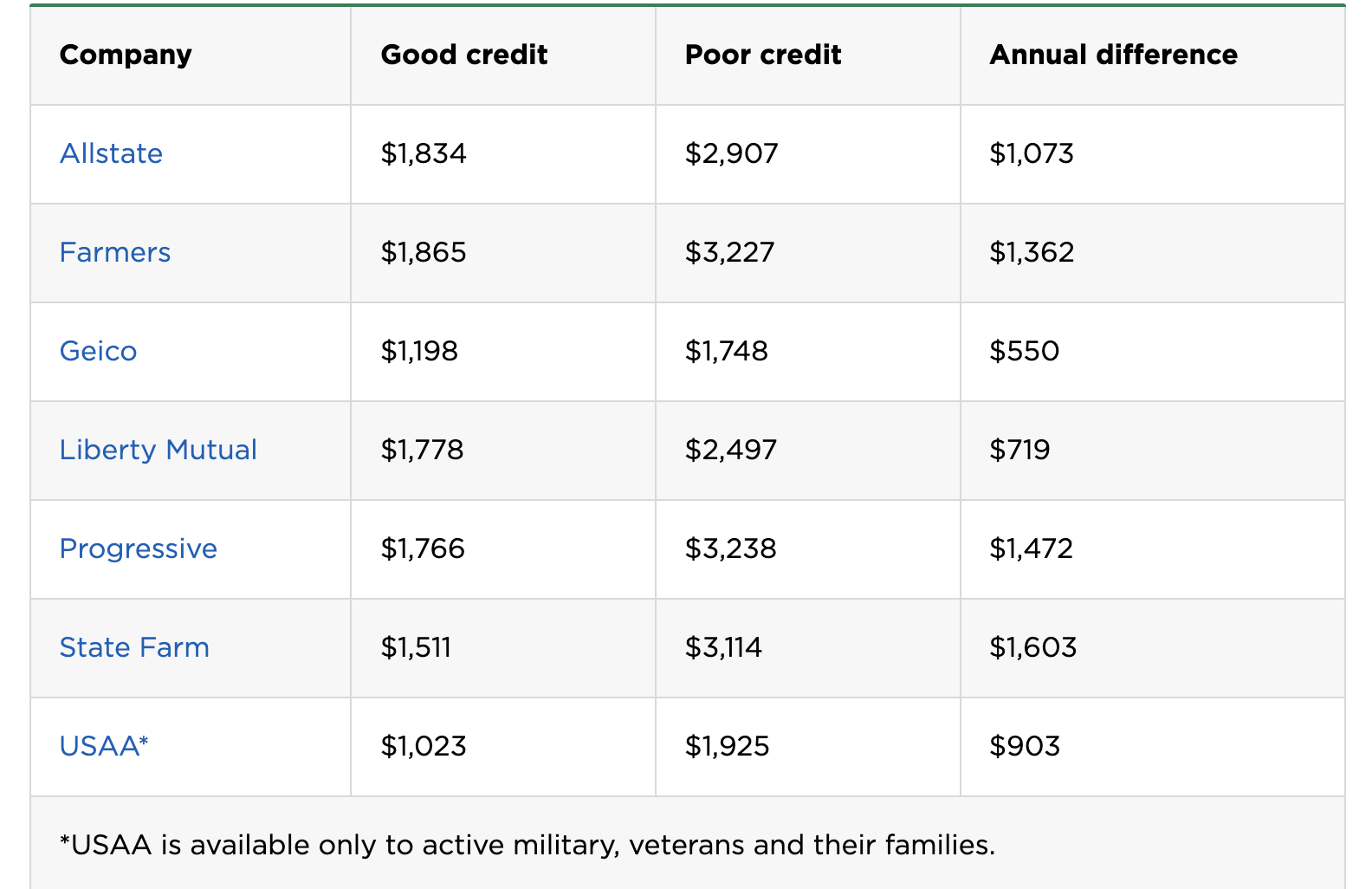

What company has the best rates for good drivers with poor credit?

Below is a table showing the list of best companies that has the best rates for good drivers with poor credit:

How to Build your Credit and Get Cheaper Insurance:

Below are a few suggestions to build your credit:

- Always try to pay down your credit balances

- Limit hard credit inquiries

- Pay off your credit card debts

- Find your credit-based insurance score

- Get a copy of your credit report.

Your credit report includes:

- Payment record

- Age of accounts

- Identification data

- Recent hard credit inquiries

- Accounts opened

- Balances

- Credit limits

- Personal details such as your job and address

- Medical debt and revolving credit

You can fall on these data to know what is affecting your credit score since both credit scores and credit-based insurance scores use the same information in different ways.

Other Ways To Save On Car Insurance If You Have Poor Credit

Scout around and compare car insurance rates. You could find a better price than what you are paying now, whether you have poor credit or not.

This is because every company weighs the factors differently. A company may raise your rate by 10% for poor credit and another company might raise your rate by 5%.

Your insurance credit score is very important especially when you’re getting a policy with the company for the first time.

Some auto insurers look at your credit every time you want to renew your policy, while other companies check occasionally. How often it is being checked depends on the state regulations.

You can’t assume you would get the best rate just because you improved your credit.

You might get lower insurance rates when using Usage-based insurance. Usage-based insurance uses factors like age and location and also driver behavior to determine your car insurance rate.

Some insurers such as Root and Progressive specialize in this option.

Frequently Asked Questions

Does getting insurance quotes to affect your score?

Scouting around for an insurance quote won’t affect your credit score in any way. A hard credit pull will occur when you apply for credit such as a credit card or mortgage.

Is an Insurance score the same as a credit score?

They both look at similar factors such as your payment history but they are totally different. Insurance companies use credit scores to predict how probable it is for you to file a claim and a poor score translates to a higher insurance rate.

What is a good credit-based insurance score?

Every insurer determines what they consider a good credit-based score. Nonetheless, your normal credit score can give you an idea of how great your insurance score is.

GIPHY App Key not set. Please check settings